Memorial Day weekend holds a special place in my heart. Sure, I say thank you to all of the veterans who were lucky to return to the United States after their service, but what about those who gave their lives so we remain free? Bless you all.

I’ll start this weekend with a few stocks that fulfill simple objectives for our portfolio, and your portfolio. Remember, we are longer-term investors than not. Sure, trading is beneficial from time to time if you have a base to work from. We place that second, but check back tomorrow as I’ll present an overview of what’s out there.

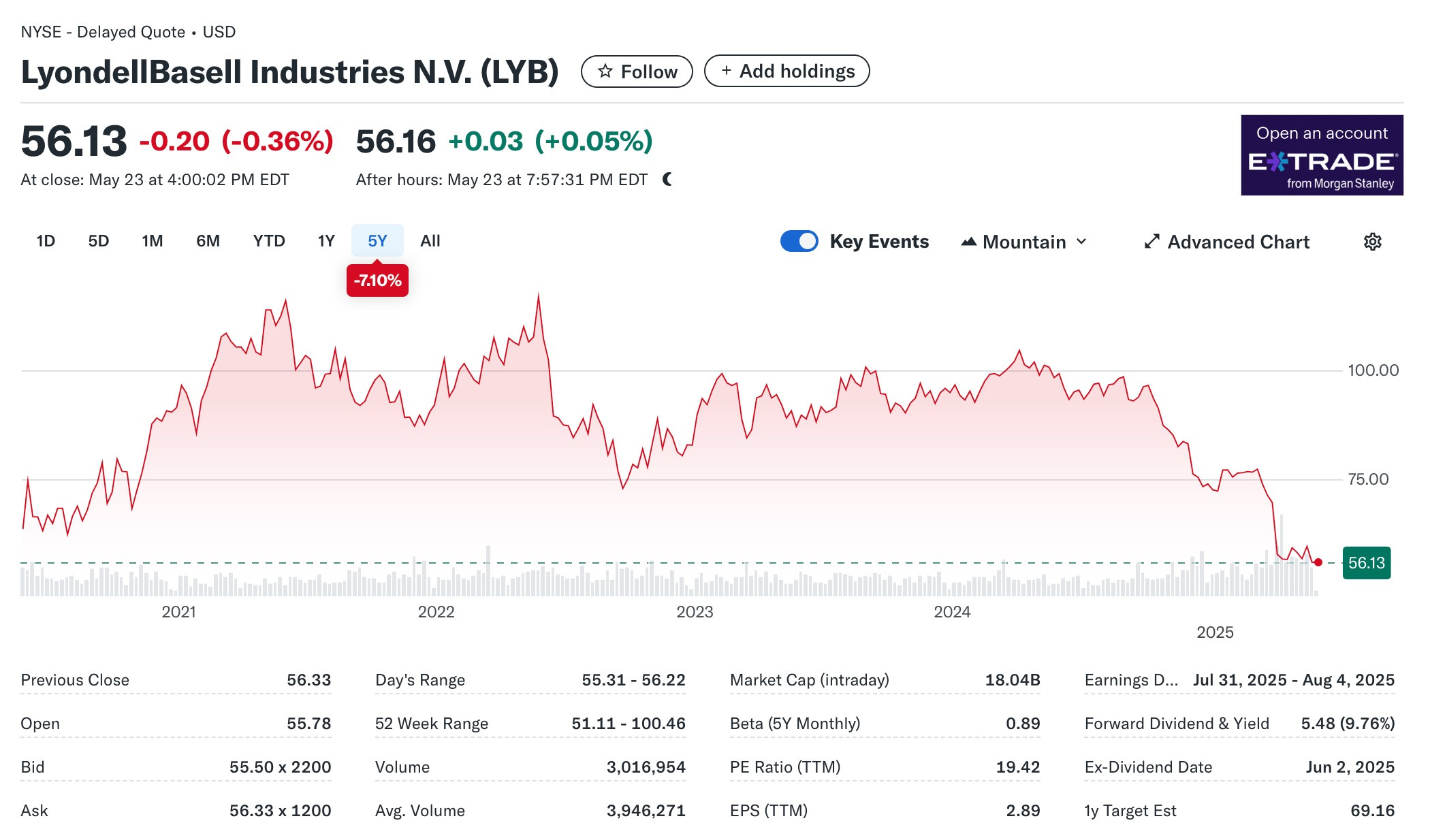

LyondellBasell Industries

LyondellBasell Industries (“LYB”) trades at $56.16, has a fair value estimate of $76.36, and yields about 9.50%. What else do you need? LyondellBasell Industries, a global leader in chemicals, plastics, and refining, is another stock well-suited for a rising yield environment. The company produces essential materials like polyethylene and polypropylene, which are critical to industries such as packaging, automotive, and construction. Higher commodity prices, particularly for petrochemicals, boost the company’s margins, as raw material costs are often passed through to customers.

It stands out for its very high shareholder yield and a 15-year streak of uninterrupted dividends. LyondellBasell currently sports a robust 9.50% dividend yield, positioning it among the higher-yield options in chemicals. The firm’s strong free cash flow yield and ongoing share buybacks add to its investor appeal.

LyondellBasell benefits from additional tailwinds that could propel its stock higher in 2025. The company’s global footprint, with significant operations in the United States and Europe, positions it to capitalize on regional demand surges.

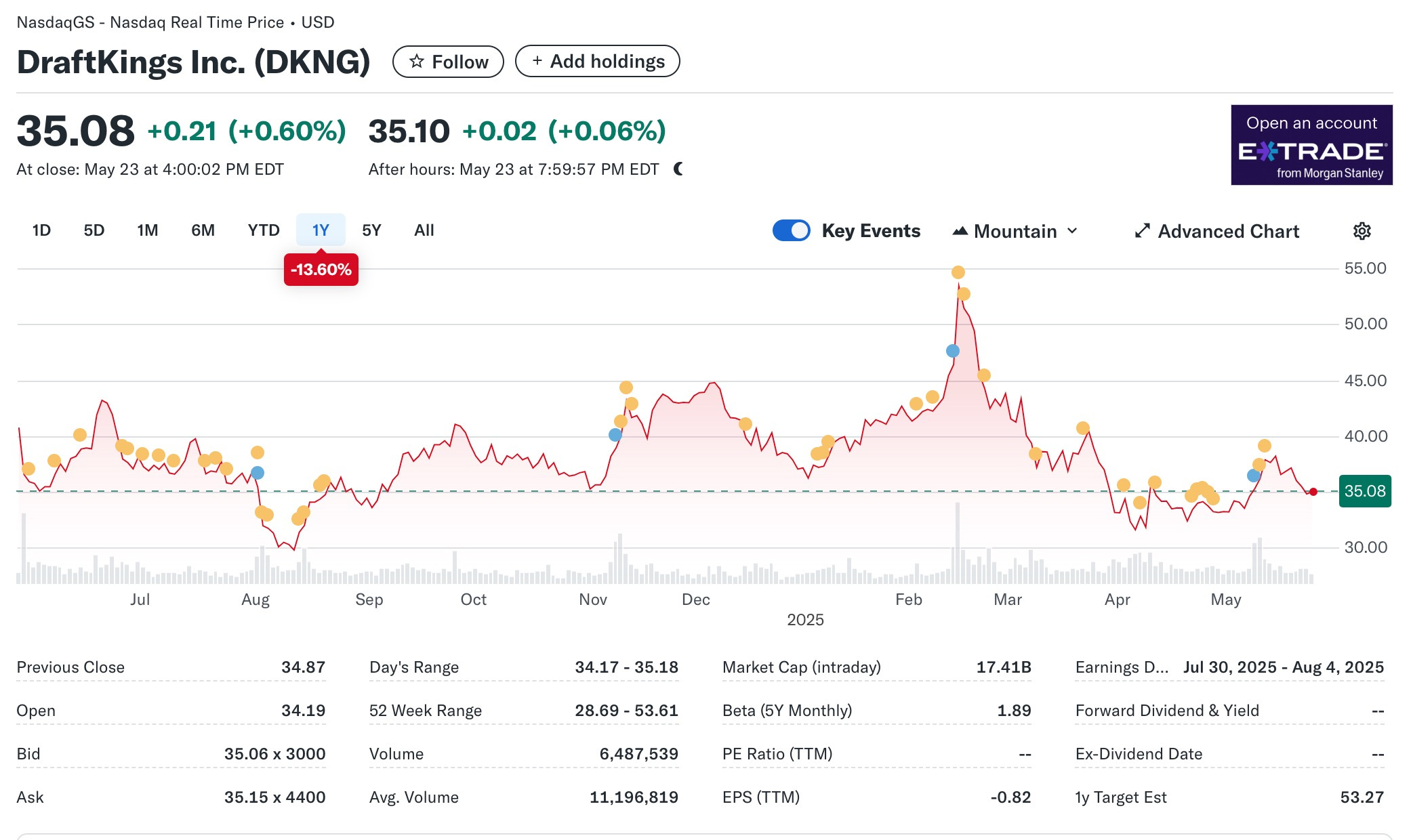

DraftKings

During an earnings season where many companies lowered their guidance, darling gambling stock DraftKings (“DKNG”) had to do just that. Even as shares are down nearly 34% from their all-time high reached in February, as of today, DraftKings stock is still up more than 150% over the past three years.

DraftKings has seen an explosive rise in the popularity of its platform over the last several years. At the end of 2020, the company had about 900,000 monthly unique payers (MUPs). This number shows how many users placed a bet on its platform in a month. MUPs have more than quadrupled since, coming in at 4.3 million in the most recent quarter. Despite this, lowering guidance is never something investors want to see. So, what is in store for this consumer discretionary name going forward?

The company also lowered its guidance by around 2% at the midpoint to $6.3 billion, equating to a decrease of $150 million. However, this news has multiple silver linings.

DraftKings tackled its weak guidance at the start of the earnings call. They said, “If not for customer-friendly sports outcomes in March, we would be raising our fiscal year 2025 revenue and adjusted EBITDA guidance.” DraftKings refers to negative betting outcomes that occurred against it during the March Madness tournament, the largest sports betting event in the United States. When most gamblers win their bets, DraftKings is on the losing end as the bookie, which is exactly what happened in this year’s tournament.

Sports bettors tend to spend more money on the favorite, or the team with a higher chance of winning, than on underdogs. Thus, DraftKings can make a lot of money when those favorites lose. However, during this March Madness, higher-seeded teams, which are typically favorites in their matchups, won their games 82% of the time. This was the highest rate ever, causing DraftKings to lose an unprecedentedly large number of bets.

The second silver lining is that DraftKings stock rose over 2% after its earnings release. This demonstrates that Wall Street wasn’t scared away by the company’s unusual plight in the quarter. Lastly, Wall Street analysts tended not to adjust their price targets significantly in response to the results.

Despite recent issues, DraftKings is still well-positioned going forward. The company grew its MUPs by a brisk 28% in the quarter, and expects its adjusted gross margin to increase by 300 basis points in 2025 over 2024. Wall Street price targets remain very bullish, and DraftKings still only offers online sports betting in around half of the U.S. states. This provides a substantial opportunity for expansion long-term.

Adobe

Adobe Inc. (“ADBE’) is a major player in the software industry, known primarily for its creative software suite (Photoshop, Illustrator, Premiere Pro, etc.), as well as its growing cloud-based solutions (Adobe Creative Cloud, Adobe Document Cloud, and Adobe Experience Cloud).

Here's a look at the stock from various angles:

Price Range (52-week): ~$420 – $635

Market Cap: ~$275 billion

P/E Ratio: ~45 (may vary)

Dividend: None (Adobe does not currently pay a dividend)

Creative Cloud Dominance

Adobe continues to dominate the creative software space. Subscription-based pricing via Creative Cloud provides predictable, recurring revenue.Digital Experience and Marketing Cloud

Adobe has expanded aggressively into digital marketing and analytics via Adobe Experience Cloud. This business complements its creative tools and provides a solid growth vector.AI Integration

With the rollout of Adobe Firefly, a generative AI tool integrated into Photoshop and Illustrator, Adobe is well-positioned to benefit from AI trends.Enterprise Adoption

Adobe's products are deeply embedded in creative and marketing workflows across enterprises, helping with customer retention and high switching costs.

Adobe’s financial strength is solid.

Strong Free Cash Flow

Adobe consistently generates billions in free cash flow annually, supporting R&D and potential share buybacks.Revenue Growth

Adobe has seen steady revenue growth, with double-digit YoY growth in recent years, driven largely by subscription services.Margins

High gross margins (~85%) and operating margins (~35%) indicate pricing power and operational efficiency.

There are always risks and challenges.

Competition

Tools like Canva, Figma (UX/UI), and generative AI competitors are threats for smaller users or startups.Valuation Concerns

Adobe trades at a premium valuation, which could be sensitive to interest rate movements or broader tech corrections.Acquisition Scrutiny

Adobe’s proposed $20B acquisition of Figma was ultimately canceled in 2023 due to regulatory hurdles, signaling challenges in future growth via M&A.

Adobe is a strong long-term play in creative software and digital experiences, with solid fundamentals and growth potential via AI and enterprise adoption. However, investors should be mindful of its rich valuation and rising competition.

And so it goes, mortality sucks. I’m 70 years old. The mind is sharper than it’s ever been, but my ability to physically handle everyday tasks is somewhat limited. I do not like what I’m hearing about a hero, Billy Joel. I first saw him playing at a piano bar in Pennsylvania. He was younger. So was I, but this song was on his mind then, and it’s on my mind now. Take care, Mr. Joel. Get better, you are missed.