Confessions Of A Currency Position Trader

If "A" Then "B" Then Possibly "C" Or "D"

Seldom do I get the chance to teach “history” with potential current “caveats” from recent events. Such is the case this week culminating in today’s preparatory article coupled with tomorrow’s “The Week That Was & What’s Next”. Understand however that we’ve got the U.S. Open in progress, and it’s a good one, coupled with “Father’s Day” so chances are tomorrow’s video is going to be published early. Always take into consideration what makes you happy in life and put it first. That’s an important part of “Building A Plan”, one of the several courses in progress here at The Ticker EDU. If you have balance in your life chances are that will emotionally overlap with balance in your investment or trading arena. It’s only natural and trust me, it works.

So we had one hell of a week, didn’t we? There weren’t really all that many surprises but there’s still a lot to learn from. If I had to give myself a title, I’m mostly a currency position trader. I’m also a long term “hedger” versus being just a short term “trader” most of that coming from clients I’ve represented and worked with for years. Futures markets did not initially come into existence because the day, scalp and swing traders needed a “vehicle to drive” themselves crazy. Commodity futures markets came into existence to enable producers, suppliers and those that bought, sold or just used their products to operate much more efficiently in their markets. Futures markets enabled them to plan, to price their products, to control their expenses. While clearing houses depend on traders to make more money by creating a varied, enhanced portfolio of products for speculators to “gamble” with, “real world” commodities remain the heart and soul of the financial system. Remember, less than 10% of all traders make money. Most hedgers, at least those who are long term, capable, solid business people, create the market and usually benefit their businesses in a positive manner. That is why I’m primarily a hedger; how about you?

China’s Impactful News Week

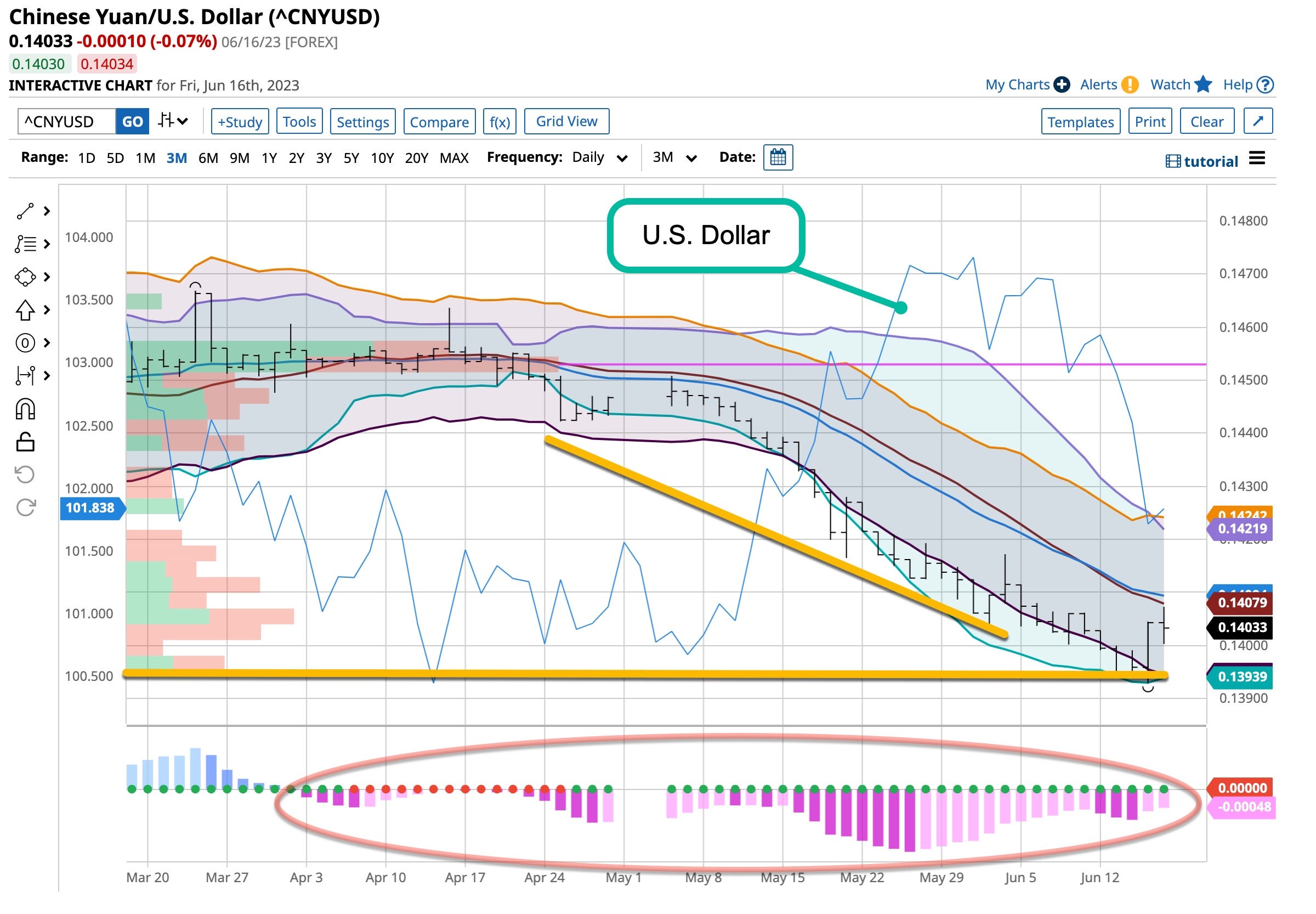

So let’s start with China. After all China does a little business with the world so there is a reason to hedge the Yuan, especially is you depend upon the Chinese market for importing products you sell. This tied to recent events, some still COVID related, are affecting not just the basic currency exchange rates between the Yuan and the Dollar, economically, money supply wise, future actions by the PBoC could affect much more. Let’s start with the currency exchange between these two currencies, with both a long term and a short term perspective.

China lowered their interest rates, the Fed paused, but it also warned of higher future rates. As expected, the Yuan decreased in value against the Dollar. Like everything in today’s market, the news was “oversold” as was the subsequent rebound but the die is cast; the Dollar is going to head higher against the Yuan regardless of heading lower against the Euro and the Pound where interest rates are heading higher..

Before digging into the potential “next steps” China may take to refund its Treasury, I suggest we dig deeper as to why and their possible effects. Cycles repeat themselves; the one we’re currently subjected to is as bad as anything I’ve ever seen. I agree with Professor Harold Hill; unless things change trouble is about to become cataclysmic.

China needs more than lowered interest rates to ignite its COVID racked economy; it needs capital. If China were to sell its U.S. bond holdings, significant implications for both China and the United States would arise. Here are some possible consequences:

Bond Market Impact: China is one of the largest holders of US Treasury bonds, and a massive sell-off could flood the market with bonds, leading to a decrease in their value. This could result in an increase in bond yields, causing interest rates to rise in the United States.

Currency Exchange Rates: Selling a substantial amount of U.S. bonds would require China to convert the proceeds into another currency, such as Chinese Yuan. This could potentially lead to a short term appreciation of the Yuan and a depreciation of the U.S. dollar in foreign exchange markets.

Increased U.S. Borrowing Costs: If bond yields rise due to a sell-off, the U.S. government would need to offer higher interest rates to attract new buyers for its bonds. This would increase borrowing costs for the US government, potentially affecting its ability to fund budget deficits and finance various programs.

Impact on US Debt: China's selling of US bonds could increase concerns about the sustainability of U.S. debt levels. It may raise questions about the ability of the U.S. government to service its debt which would lead to a loss of confidence in the U.S. financial system.

Diversification of China's Reserves: Selling US bonds could be part of China's broader strategy to diversify its foreign exchange reserves. By reducing exposure to U.S. debt, China could allocate its reserves to other assets, such as gold, other currencies, or investments in other countries.

Geopolitical Tensions: The sale of U.S. bonds by China could very well be seen as a political move, potentially escalating geopolitical tensions between China and the United States. It might be interpreted as a signal of strained relations, leading to further trade disputes, financial repercussions and greater uncertainties about Taiwan.

It's important to note that the actual consequences would depend on various factors, including the scale and pace of the bond sales, market reactions, and the response of policymakers. I sense if something of this nature materializes the “big boys”, Goldman Sachs, J.P. Morgan and the like will essentially treat such a sale of this nature like a “secondary offering” ensuring its success while minimizing the damage to the market. Now what would happen if China doesn’t stop here and looks to “liquify” some of its stockpile of gold?

If China were to sell a significant portion of its gold holdings, it could have several implications for the global economy and financial markets. Here are some possible consequences:

Gold Market Impact: China is one of the world's largest holders of gold reserves. A large-scale sell-off could flood the gold market, leading to a decrease in gold prices. This could have a significant impact on the global gold market and affect investor sentiment.

Currency Exchange Rates: Selling a substantial amount of gold could result in China converting the proceeds into another currency, such as the Chinese Yuan. This could potentially lead to a short term appreciation of the Yuan coupled with a depreciation of the currency in which the gold is sold, the U.S. Dollar, Euro and perhaps the Pound and Swiss Franc.

Investor Confidence: China's decision to sell a significant amount of gold could be interpreted as a lack of confidence in the precious metal as a safe-haven asset. It might raise concerns among investors about the stability of the global economy or the financial system, leading to increased market volatility and risk aversion.

Impact on Gold Prices: A substantial sale of gold by China could put downward pressure on gold prices, at least in the short term. The extent of the impact would depend on the scale of the sell-off relative to the total gold market and the other market dynamics at play at the time of the sale.

Central Bank Behavior: China's sale of gold reserves could influence the internal behavior of other central banks and governments. If China's move is perceived as a signal of changing sentiment towards gold, it might prompt other countries to reevaluate their gold holdings and potentially follow suit, further impacting gold prices and general economic market dynamics.

Economic and Geopolitical Implications: The decision to sell gold reserves could have broader economic and geopolitical implications. It might very well signal a shift in China's economic or financial strategy, such as a need for liquidity or a reallocation of assets. It could also impact China's position in international trade or diplomatic relations, depending on how it’s interpreted by other countries.

It's worth noting that the actual consequences would depend on the scale, pace, and context of China's gold sales, as well as market reactions and the actual response of other market participants.

As time allows tomorrow, I’ll do my best to address additional “relationships” based upon the Dollar’s movement with respect to other commodity contracts like the Yen, 30-year bonds, corn and soybeans. These charts will appear on a second post as space is somewhat limited to depict them all accurately for Sunday’s “The Week That Was & What’s Next”.

Remember, I’m just a “young” 68 years old and trust me, it was good to get a solid night of sleep. Looking forward to the weekend’s U.S. Open and being able to teach you better how to be the best damn investor or trader you can possibly be.

Everyone learns at their own pace. If you pick everything up the first time through, great but if not email me at david@thetickeredu.com so we can further help. Again, let me know what you want to learn, I’m all ears.

Finally an Elton John song that fits. “Saturday Night’s Alright For Fighting” suits the topics well. Whether perceived by the overall populous or not the United States is in a dogfight with China. China’s economy is sneezing and unlike in the past, China’s now large enough to infect the world. Becoming dependent manufacturing wise was not a good strategy and the world is about to pay for it. Time to make some changes and to perhaps set in motion a different plan of “attack”.